Do you know how much you’re paying in investment fees each year?

If you’re like most people, chances are you don’t. And not paying attention to those fees is taking years off of your retirement.

Expense Ratio

Most mutual funds and exchange-traded funds (ETFs) charge an annual fee as a percentage of assets. This means that each and every year your account is charged whether the fund makes money or not.

This fee is called an expense ratio. Funds are required to disclose this information and you can use sites like Morningstar to research what each mutual fund charges.

There are two types of expense ratios that can be reported – an annual gross expense ratio and an annual net expense ratio.

The annual gross ratio includes the percentage of assets used to pay for all of the fund’s expenses. These can include interest expense, legal & audit fees, and expenses for the day-to-day operation of the fund.

While similar to the annual gross ratio, the annual net ratio includes expenses for day-to-day operations and various legal & accounting fees. The main difference is that it does not include interest expense or the fund’s brokerage costs.

When reviewing your mutual fund’s fees and expenses, stick with the annual gross ratio. It’s a more complete picture of what your fund is actually charging.

Investment Advisor Fees

Mutual fund fees are only part of the picture. Many of you also have a financial advisor.

These independent financial advisors charge fees as well, for helping you manage your investments. Since they are only helping you manage your investments, their fee is in addition to any fees charged by the mutual fund.

Advisors typically operate on either a commission, fee-only or fee-based model.

The commission model is what most of you who use online brokers are used to. Any time you buy or sell an investment you’re charged a fee. While online

brokers like E*TRADE or TD Ameritrade charge a flat rate, an investment advisor’s commission can vary (sometimes as high as 3-4 percent) based on the product. This can create major conflicts of interest, since they have an incentive to sell you the product that will pay them the most, not what is necessarily best for your portfolio.

Under a fee-only model, investment advisors are paid a flat percentage of your assets each year. This is similar to how mutual funds and ETFs collect fees. You aren’t charged based on the number of transactions or the products you invest in. Instead, you’re charged based on your total assets under management.

According to a study performed by the Registered Investment Advisor, the average financial advisor fee was 0.99 percent.

With a fee-based pricing model, advisors can be paid either by commissions, a percentage of your assets or both.

Why Don’t You Pay Attention to Fees?

I’ll be the first to admit, that until recently, I never really paid much attention to fees. And that got me thinking – why is that? Why do most people ignore fees when selecting mutual funds or reviewing their annual performance?

I think the answer lies in your perspective.

The average mutual fund fees were approximately 0.57 percent in 2016. When most people see this, they just assume that half a percent isn’t large enough to worry about. Plus, the mutual fund companies just deduct these fees from your returns. So, at the end of the year, when you see your fund was up 8 percent, you consider it a good year, instead of thinking you could have made 8.25 percent with a less expensive fund.

When it comes to investment advisor fees, most people feel that the fees are unavoidable. If you find an advisor that you like and is helping you make money, paying a percent or two may seem like a reasonable trade off.

While these fees are unavoidable if you want an advisor, that doesn’t mean you should blindly pay what they charge. If you pay by commission, switch to a fee-based model. It will most likely be cheaper, plus it eliminates that pesky conflict of interest. Or talk to other financial advisors and see what they charge. Chances are you will be able to find an advisor with lower fees or you could use that research to negotiate a better arrangement with your current advisor.

Fees are the Enemy of Retirement

While all of these investment expenses may not appear to be much, paying higher fees is actually costing you years off of your retirement.

Let’s say you fully fund ($5,500) your IRA each year. You’re deciding which mutual fund to invest in so you compare the fees. They both have similar returns (for simplicity), but one has an expense ratio of 0.75 percent (Fund A), while the other’s is only 0.25 percent (Fund B). A half of a percent may not seem like much but over time those additional fees compound into a significant sum.

Now assume both funds earn 8.25 percent per year. This means that Fund A will net you 7.50 percent after fees while Fund B would be 8.00 percent. After 30 years, you would have $569,000 with Fund A. At this point, you’re probably thinking how great that sounds, but let’s look at Fund B.

The additional 0.50 percent really adds up over 30 years. At the end of this time period, Fund B would have $623,000 or $54,000 more than Fund A!

| Fund A | Fund B | |

| Net Return | 7.50% | 8.00% |

| Annual Contribution | 5,500 | 5,500 |

| Ending Balance | $ 569,000 | $ 623,000 |

| Difference | $ 54,000 |

That difference alone is at least a year of retirement. But don’t forget that the difference continues to compound even once you do retire. In your first year of retirement Fund A would earn you around $43,000 whereas with Fund B you would have closer to $50,000.

Even More Fees

The above example only factored in mutual fund fees. But if you factor in the fees for financial planning, the impact to your retirement is even greater. Since advisors typically charge higher fees than mutual funds, there is a greater range in their expenses. While the average financial advisor fee is around 1 percent some investors are paying closer to 3.5 percent.

With such a wide range, let’s assume the difference in total fees (both advisory and mutual fund) from Advisor A and Advisor B is 1.50 percent. Again, to most people this may not seem like much and therefore they won’t really pay attention to the fee difference, by over time it really adds up.

In this case, with a 1.50 percent fee difference, you’ll earn 6.50 percent with Advisor A and 8.00 percent with Advisor B. After 30 years of $5,500 contributions you’d end up with $475,000 with Advisor A. This is a sum of money that most people would love to have in retirement. But for the same time period and contribution amount, you could have had $623,000 with Advisor B.

The difference of $148,000 could be the difference between retiring early or having to work into your sixties. In fact, it would take an extra 4 years with Advisor A to match the same balance you’d have with Advisor B after 30 years.

| Advisor A | Advisor B | |

| Net Return | 6.50% | 8.00% |

| Annual Contribution | 5,500 | 5,500 |

| Ending Balance | $ 475,000 | $ 623,000 |

| Difference | $ 148,000 |

Again, this difference in investment expenses continues to be magnified with each passing year. In year 31, you would earn a little less than $31,000 with Advisor A. But with Advisor B you would earn closer to $50,000.

How to Reduce Your Fees

Now that you understand the impact fees have, you may be asking how can I reduce the fees I’m paying?

If you use a financial advisor a great first step would be to review your fee arrangement with him/her. Are you paying commissions or strictly a percentage of your assets? If you’re paying commissions, I would recommend first switching to a fee-only payment structure.

You can also shop around to find the best value. If you’re paying your advisor 2-3 percent they better be earning you a significantly higher return (chances are they aren’t) to justify a management fee that is 2-3 times higher than average. If you’re paying a higher than average fee to your investment advisor, try negotiating with them. Chances are your advisor will want to keep your business and will be willing to lower what they charge you.

A great way to reduce your mutual fund fees is to make sure you’re invested in passive or index funds.

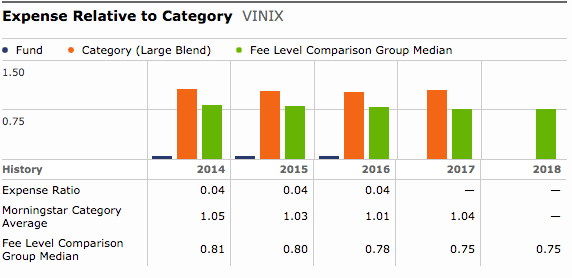

Passive funds are less expensive than actively managed funds because they typically just track an index instead of having investment managers picking stocks. Since they don’t need to pay these high-priced managers, the overall expense ratio is significantly lower. For instance, Vanguard S&P 500 Index Fund has an expense ratio of 0.04 percent versus a median of 0.81 percent.

Track Your Fees with Personal Capital

If you don’t want to look up the fees for all of your mutual funds individually, Personal Capital offers some incredibly easy to use dashboards to see your investment fees and their impact all in one place.

Personal Capital is one of my favorite personal finance apps to track all of my accounts and budgets in one place. It’s completely free to sign up and use. If you don’t have an account yet, you can sign up using this link or check out my step-by-step guide to setting up your account in under a minute.

Once you have your account setup, just go to Planning -> Retirement Fee Analyzer. From this dashboard, it’s really simple to see the impact fees have on your retirement.

Learn From My Past Mistakes. Get Your Copy of the 9 Most Common Investing Mistakes.

Get My CopyRetirement Fee Analyzer

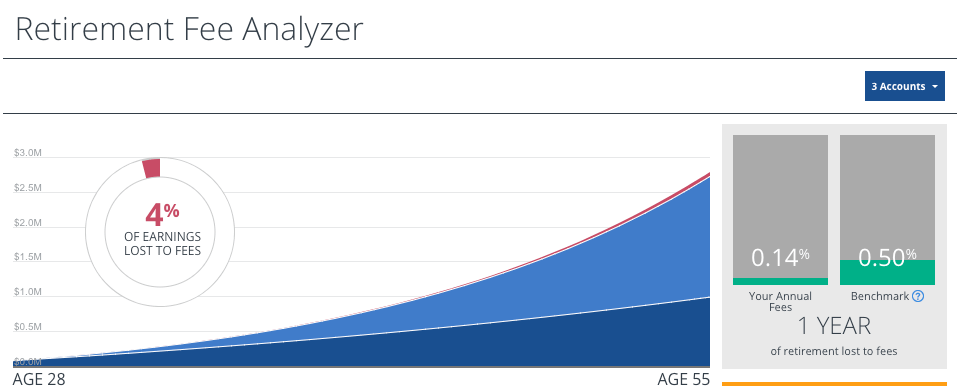

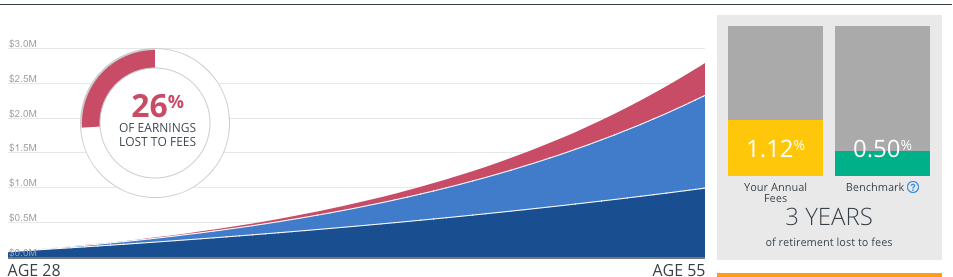

The first chart you’ll see is the Retirement Fee Analyzer. This is an awesome way to visualize the impact investment fees have on your retirement.

As you see from the image above, Personal Capital combines all the fees you’re paying and creates your total expense ratio. Plus, it gives you a benchmark for comparison.

Since thinking in terms of percentages can sometimes be difficult to grasp, the dashboard makes the numbers more concrete. It displays how many years of your retirement are lost due to fees.

If you want to add advisory fees, there is also a place for you to edit your assumptions.

This way is much easier to see how quickly, even relatively small percentages, can add up. An additional 1 percent in fees added two years of lost retirement. Plus, 26 percent of my earnings would have been lost to fees.

Expense Ratio Comparison

The second portion of the retirement fee dashboard deals with your specific investments. Here you can quickly see the individual companies or mutual funds you own along with their expense ratios.

In addition, Personal Capital multiples that ratio by your value to display your yearly fees in total dollars.

Having this information easily accessible makes it much easier to keep track of your overall fees. It also helps you make targeted changes to lower your overall fees.

By seeing the total dollar amount of management costs, you pay per fund, you can target your most expensive investments first.

Try finding funds that have a similar investment profile but maybe are passive funds instead of active ones. Simply making the switch from active to passive could save you thousands of dollars in expenses over the long-term without sacrificing overall performance.

Stop Losing Your Retirement

Paying investment fees are inevitable, especially when you invest in mutual funds, and an argument could be made that paying higher fees is worth an above average return. But by and large, your goal should be to pay as little in fees as possible – by mutual fund and investment advisory. If you don’t it might just end up costing you your retirement.

Have you paid attention to the fees you paid in the past? Will you start now? Let me know in the comments.

Leave a Reply