Financial Statement Analysis

Financial Statement Analysis

When it comes to investing, it is important that you understand the financial information or fundamentals of a company before making any decisions. Assuming you don’t just want to in an index fund, you need to have some basic knowledge of a corporation before buying its stock.

However, due to the volume and complexity of the financial information that companies produce it can be difficult to know what information is important.

Having worked in public accountant as a CPA, I’ve reviewed my fair share of financial statements. My goal for writing this was to create a comprehensive guide for the average investor. With that comes the caveat that this is one LONG post! I’d recommend bookmarking it, so you can read it over a few days or easily refer back to it the next time you’re analyzing a potential investment.

This post will cover the basic financial statement analysis and get you familiar with the key numbers you should focus on.

Learning how to navigate different companies’ statements and find this information will take some time, but it will help you make smarter investing decisions. This is the first step. Once you learn the details you can move on more advanced fundamental techniques like ratio analysis.

For each post, I’ve used Facebook’s 2017 10-K. If you want to jump to a certain section you can use the links below.

Management Discussion and Analysis

Report of Independent Registered Public Accounting Firm

Statement of Income and Earnings per Share

Overview

The Securities and Exchange Commission (SEC) requires every publicly traded company to prepare a variety of financial reports.

You can easily access all of these reports through the SEC’s database.

The main reports are the 10-K and 10-Q. The 10-K is the audited annual financial statement and the 10-Q are the quarterly financial reports. These statements are prepared according to Generally Accepted Accounting Principles (GAAP).

Don’t worry about the specific GAAP requirements, just know that they are standards created by the Financial Accounting Standards Board (FASB) that all public companies must follow. They outline the disclosure requirements and provide for standard recording of transactions. Without GAAP, companies would be able to account for transactions however they wanted which would make it nearly impossible to compare two companies in the same line of business. It’s because of GAAP that investors have the information and transparency they need to make sound decisions.

Both the 10-K and 10-Q contains the main financial statements (balance sheet, income statement and statement of cash flows) along with commentary from company’s management and notes supporting significant transactions or impacts to the business.

In addition, the SEC requires companies to file a DEF 14A or Definitive Proxy Statement. This contains information that shareholders need to make informed decisions about the company. It also contains compensation information for the highest five paid employees.

Management Discussion and Analysis

When reviewing a company’s financial statements, it’s important to read through management’s comments. Since the SEC requires a company to disclose information critical to its value, you can gain a lot of valuable information from management’s commentary.

In this section, you will find an overview of the company’s business along with any major changes that may impact their financials going forward (such as a merger of acquisition).

In Facebook’s 10-K, they provide an overview of the competitive landscape as well as risks related to their business. Not only can this information be beneficial for learning more about the company you’re researching, but it can also help you gain a better idea of the industry it operates in. Facebook also provides select financial results and performance metrics in their discussion. These are typically the metrics that financial analysts look at when reviewing a company.

Report of Independent Registered Public Accounting Firm

Before you get to the actual financial statements, you come across the audit report. This is a one to two-page document prepared by the public accounting firm that audited the company, in Facebook’s case it was Ernst & Young.

These reports are basically made up of boilerplate language, so there’s no need to read the entire thing. The only paragraph you really need to pay attention to is the paragraph that contains the audit opinion.

There are four main opinions an auditor can give, unqualified, qualified, adverse and disclaimer. Leave it to accountants to come up with the four most confusing terms!

Audit Opinion Breakdown

An unqualified opinion is the best one an auditor can give. Basically, this opinion states that the auditor did not find any material issues and that the financial statements are presented fairly. Facebook’s opinion was unqualified.

The key wording to know it’s an unqualified opinion is in the second sentence – “In our opinion, the financial statements present fairly, in all material respects. . .”

A qualified opinion is used when the financial statements are presented fairly except for a certain matter or issue. In these types of opinions, there is usually another paragraph that describes the issue at hand. While this opinion is not as good as an unqualified one, it still is not terrible.

The last two opinions – adverse or disclaimer – mean that something is significantly wrong with how the financial statements are presented.

For an adverse opinion, the auditor is saying that in their opinion the financial statements are not presented properly.

A disclaimer is even worse. In this case, the auditor was not even able to express an opinion on the financial statements. If you would like to read more about audit opinions (because who wouldn’t? 😜) you can check out the AICPA.

What’s an Audit Entail?

A quick side note about audited financial statements. A lot of people think that if a company is audited then they are free from fraud or any issues. That’s simply NOT the case! Having been an auditor in a past life, I know it’s impossible to review every transaction. Just image looking through every sale Amazon makes in a year!

To get around this, auditors rely on the concept of materiality. Essentially this is a way to assign a threshold to what they review. It’s the idea that small misstatements won’t have a major impact on an investor’s decision. Only the items that could potentially mislead investors are considered material. Facebook misclassifying a few hundred thousand dollars in expenses isn’t material. But them inflating revenue by a few million dollars would be.

This coupled with statistical sampling allow them to focus on high-risk transactions. Through this testing, auditors “gain comfort” that the company recorded everything properly. The audit opinion states “in all material respects” since the testing only looks for material issues.

This isn’t to say that you shouldn’t rely on the audit opinion, but just be aware it’s not a blanket statement of financial health. Companies who receive unqualified opinions can still be bending accounting rules.

Track Your Net Worth - Sign up for Personal Capital for Free!

Financial Statement Notes

After reviewing Management’s discussion and analysis and the three main financial statements, the last section you should review is the Notes section. Since the SEC requires a great deal of information to be available to all investors, these sections are usually very detailed.

This section can vary greatly from company to company, depending on the industry and activities of the company. The notes are where a company will describe its accounting policies or provide additional detail on certain transactions or balance sheet items.

While they may not seem important, having a better understanding of how a company records certain transactions, especially sales, is crucial. In investing, it is important to have an understanding of how the company works. This includes not only the product it makes or the service it provides but also how it accounts for them in its financial statement.

Gaining a better understanding of how it records revenue or certain expenses can help you better predict what future revenues or expenses will be. And since the stock price is often based on sales growth, understanding how and when a corporation books its revenue can help you make more informed investing decisions.

Balance Sheet

Now let’s start getting into the financial statements themselves.

As I mentioned earlier, each 10-Q and 10-K contains a balance sheet, income statement, and statement of cash flows. Each of these statements tells a different part of the company’s overall financial story.

The balance sheet is broken up into three main sections: assets, liabilities, and equity.

The balance sheet provides a look at the company as of a point in time. The date of the balance sheet is either the end of the quarter or year. All of the information provided shows the balances for each item as of that date.

While this is important information, just remember that balances change every day. While a company may look good or bad on a certain day, you need all of the financial statements to get a true picture.

Assets

A company’s assets are very similar to an individual’s assets.

They are made up of all the items that can be used to create revenue or grow the business. Facebook, for example, lists items like cash, accounts receivable, and property as some of their assets.

Tangible vs. Intangible

All of these assets are tangible, meaning that they physically exist. But you will notice that Facebook also lists intangible assets.

Intangible assets include trademarks or goodwill.

Goodwill is created by buying a company and paying more than the physical assets are worth. For instance, if Facebook buys a company for $1 billion, but the company only has physical assets worth $900 million, Facebook would be paying $100 million in goodwill.

Companies often pay more for another company because of the added value it will bring to their business either through new technology or new customers. That’s why goodwill is classified as an asset. The logic is that the extra money you’re paying is for some future value or revenue to your business.

Current vs. Non Current Assets

Assets are also broken down into current and non-current or long-term. On the balance sheet, assets are listed in terms of their liquidity (or how quickly they can be turned into cash). So current assets are listed first, followed by long-term assets.

Current assets are ones that can be used within one year (twelve months) of the date of the financial statements.

Cash is a current asset because it can be used to purchase something at a moment’s notice. There is no need to hold on to cash for two years before you can use it for purchases. Customer receivables are typically current as well since they are expected to be paid within one year.

Long-term assets can’t or won’t be used within one year. Investments that must be held for longer than a year (such as investments in other companies) are classified as non-current.

Goodwill is also a long-term asset since you expect the benefits of buying a company to last longer than a year.

Property and equipment are a great example of a long-term asset. When you buy a piece of equipment you expect it to last multiple years, not just one. Due to the nature of non-current assets, a company with a majority of their assets in long-term could still potentially face short-term financing issues as they may not have the funds available to operate the business on a day to day basis.

Equipment is Capitalized

Just a quick note on capitalization of property and equipment. You may be wondering why something like equipment would be listed as an asset and not an expense. This is because the equipment is capitalized when it is purchased.

This means that no expense is recorded when it is purchased, but rather it is expensed (through depreciation) over the amount of time you expect to use it.

This is due to an accounting practice called the matching principle. I won’t get into it too much here, but its main goal is to match revenue with the expenses used to earn that revenue.

Since you purchased equipment in one year, but use it over five to ten years, in order to correctly match the expenses to the future revenue you will make by using the equipment, you capitalize the asset and expense a little bit each year.

Learn From My Past Mistakes. Get Your Copy of the 9 Most Common Investing Mistakes.

Get My CopyLiabilities

Moving down the balance sheet, liabilities are the next main section. They are organized very similar to assets, with both having current and non-current sections. One main difference is that there really aren’t any sort of intangible liabilities (at least none that I have come across).

Current liabilities are the payments that a company is going to have to make within the next twelve months. Accounts payable and current payments on debt are the main items here.

Corporate Credit Card

Think of accounts payable as owing money on your credit card. When you buy something on your credit card, you purchased the item, but really didn’t pay any cash for it. So while you have the cash, you now owe money to the credit card company.

Companies do the same thing but without credit cards. When companies purchase materials from suppliers, they usually buy it on their account. This way they have more time (usually 30 or 60 days) to pay for it. In order to accurately reflect this future liability the amount gets recorded in accounts payable.

Current vs. Non Current Liabilities

The current payments on debt are shown to illustrate the debt payments the company is required to make within the next twelve months.

Non-current or long-term liabilities, like long-term assets, are liabilities that won’t be paid within the next year.

This could really be any commitment the company has that’s over a year, but the main one is debt. While the payments for the next twelve months are listed as a current liability, the remaining payments are all listed as long-term. In order to get the total debt a company has, you need to add the two together.

Some other items that companies may classify as a non-current liability include deferred compensation or deferred revenue.

Deferred revenue is revenue the company has received for a product but hasn’t earned since it has not fulfilled its obligation. An example would be if you sign up for a two-year magazine subscription. At the time you sign up the company received payment for two-years, but hasn’t delivered a single magazine (the product you ordered).

Therefore, it hasn’t fulfilled its obligation of providing 24 magazines. Since it hasn’t delivered a magazine, it can’t record your payment as revenue. Instead, it records it as a liability or future obligation and then as it sends you a magazine, it moves 1/24 from deferred revenue to actual revenue on the income statement.

Equity

The equity section is a major area for investors since it essentially outlines how much the company is worth.

This section shows the initial value of stock sold plus any past earnings (called retained earnings) that still remain in the company. Due to the accounting principle that assets must equal liabilities plus equity, the total equity in the company is simply the assets minus the liabilities.

So, if a company has more liabilities than they do assets, the equity is negative and the investors stock is essentially worthless (which is what happens in bankruptcy situations).

Market Cap

While equity does show the net worth of the company, it does not equate to what the value of the stock is worth.

Remember that stock is only a piece of paper. It represents what people believe a company is worth, not what the actual equity is in a company. Companies on the Dow have market caps numerous times higher than their actual equity.

Facebook’s total equity was around $74 billion dollars, while at the same time their market cap was 6-7 times that. While having positive equity is a good sign of financial strength, remember that stock prices don’t equal equity.

Statement of Income and Earnings per Share

The next portion of the financial statement is the statement of income. While the balance sheet provides a point in time review of a company, the income statement shows the results of a company’s operations over a certain time period. The time period is usually for 3, 6, 9, or 12 months depending on if they are a quarterly or yearly statement.

Overall, the statement of income is much simpler than the other two statements. Essentially, the statement lists a company’s revenues, expenses, and net income.

Revenue

Looking at Facebook’s statement of income, they show one line for their total revenue. Now a major corporation like Facebook has multiple revenue streams, but on the statement of income, they are all listed on one line. If you want to know what the significant sources of revenue are, you need to look in either the management’s discussion and analysis or the notes to the financial statements.

Expenses

Next Facebook lists out their expenses and here they breakout a few major categories – cost of revenue, research and development, marketing and sales, and general and administrative.

The cost of revenue are any costs that can be directly related or needed to earn their revenue. In Facebook’s case, this probably includes salaries and costs related to selling advertisements on Facebook.

Research and development and marketing and sales are costs directly related to developing new products and marketing the company.

General and administrative sounds a bit more abstract. These are all of the costs that don’t directly relate to one of the other specific areas. They are usually costs that support the whole organization. For instance, Facebook’s payroll and benefits for their accounting department would be included in these costs. They support the organization as a whole and are not directly involved in selling or developing products.

Earnings for Investors

After the income from operations, any interest expense or income taxes are lists to arrive at the company’s net income. This is the income that is theoretically available to the company’s shareholders.

I say theoretically because the shareholders don’t actually receive this money unless the company pays them a dividend. More likely than not, this income will stay with the company (in the form of retained earnings) to help fund future growth. The amount of income each share of stock outstanding earns is listed as earnings per share.

![]()

Calculating Earnings per Share

The earnings per share is calculated by taking total net income and dividing it by the average number of shares outstanding during the time period.

As you can see with Facebook’s earnings per share, there are two types: basic and diluted.

Basic earnings per share are what I just described. Diluted earnings per share takes into account outstanding stock options when determining the outstanding shares for the time period.

If a company has 100,000 shares outstanding but has issued stock options that can be converted into another 50,000 shares, it adds the additional shares to the actual outstanding shares to determine the diluted earnings per share. In this example, the company would take its net income and divide by 150,000 shares.

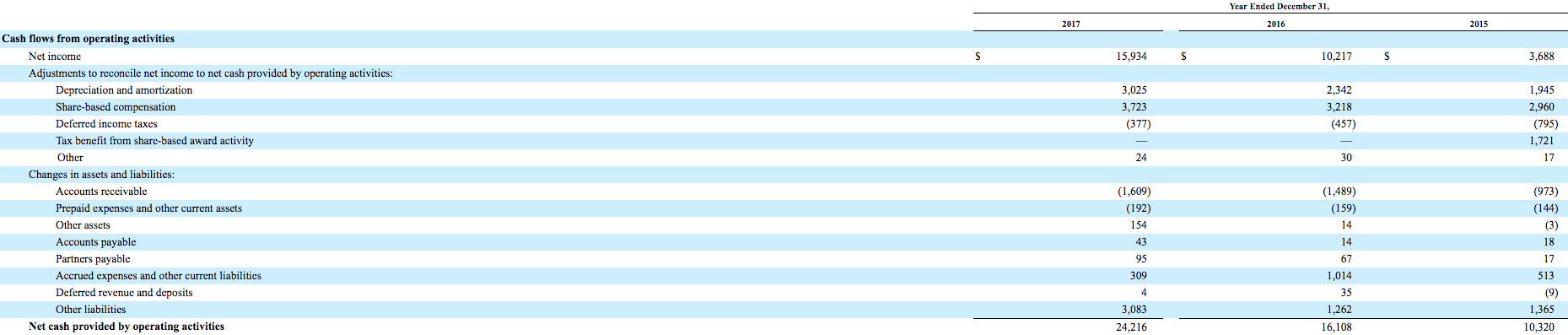

Statement of Cash Flows

The last statement of the main financial statements is the Statement of Cash Flows. While the Statement of Income shows how much the business earned in a year, the Statement of Cash Flows shows how much cash it gained or lost.

The Statement of Income is on an accrual basis. Due to the matching principle companies will capitalize costs in one year and expense them in future years. A company could spend millions of dollars in one year, but that expense will not appear for years.

The Statement of Cash Flows, however, would show that cash outflow in the year it occurred. You can think of the Statement of Cash Flows as a leading indicator. If a company is showing net income each year but is losing cash from operating activities each year, eventually those costs will catch up and they will start showing losses on the Statement of Income.

Cash Flow from Operating Activities

The first section of the Statement of Cash Flows is the cash flow from operating activities. This section essentially reconciles net income from an accrual to a cash basis.

Direct and Indirect Method

There are two methods for calculating the cash flow from operating activities, the direct and indirect method. The different methods only impact the operating activities section. Both the financing and investing activities are calculated the same way no matter which way a company uses for the operating activities section.

As you can see from Facebook’s statement, this section starts with net income for the period. From there it factors in various adjustments to arrive at cash provided by operating activities. This is the indirect method. This method is the most common for companies because if they use the direct method, they must provide an additional reconciliation essentially showing the indirect method as well.

The main difference between the two methods is that the indirect method starts with net income and adjusts to cash provided by operations; whereas the direct method simply lists all sources or uses of cash, such as collections from customers or payments to suppliers.

Adjustments to Cash

The first set of adjustments are considered non-cash items.

These adjustments are expenses taken in the current year in which cash was not actually paid. The first one listed is depreciation and amortization. Since the equipment is paid for in one year and expensed via depreciation later, the year in which depreciation expense impacts net income, no additional cash actually was paid. Therefore the depreciation and amortization expense is added back to net income, as well as the other adjusting items.

The next section of adjustments lists changes in balance sheet accounts.

Changes in Liabilities

Let’s look at accounts payable. When Facebook makes a purchase, the expense is recorded on the Statement of Income. However, companies do not always pay for an item right away. If they do not pay cash right away, they have created a payable. When the cash is finally paid, no additional expense is recorded, but cash is used up. So in order to arrive at the cash provided or used by operations, one must adjust for the change in accounts payable.

If accounts payable decreases, then cash is used and the adjustment is negative. Conversely, if accounts payable increases then the adjustment is positive since the expenses recorded in net income did not lower the cash balance. Therefore, those expenses need to be reversed in order to arrive at the cash balance.

This is true for all liability accounts. If the account decreases then cash was used, but if it increases, it is the same as getting cash since you’re deferring payment.

Changes in Assets

The opposite is true for asset accounts, like accounts receivable. If an asset account increases, then cash is used since an asset is something that can be converted to cash at a later date. An increase in accounts receivable would mean that you essentially funded a customer’s purchase with your own cash. However, once you’re paid, the receivable balance decreases and you now have the additional cash in your account.

In total, the Cash Flow from Operating Activities shows whether the company is making any money. If the company is consistently showing negative cash from operating activities, that should be a warning sign to investors.

It means that the basic operations of the company aren’t profitable. They probably won’t be able to pay dividends. In fact the company will need to raise cash just to sustain the business.

Cash Flow from Investing Activities

Cash flow from investing activities is the next section in the Statement of Cash Flows.

This section deals with changes in non-operational assets.

Two examples are purchases/ sales of equipment, as well as acquisitions of other businesses. One item to note with equipment, if it was purchased using debt, the resulting increase in debt would not be shown in this section. Instead, it would be in the cash flow from financing activities.

Cash Flow from Financing Activities

The cash flow from financing activities lists any changes to related to the financing of the business.

This includes loan payments made during the period or cash received from taking on new debt. In addition, any changes to equity are included in this section as well. These changes include paying dividends or issuing or buying back the company’s own stock.

Consistent losses in cash from operations that are offset by increases in cash from financing activities may be indicative that the company is using debt to finance ongoing losses and could potentially be a red flag.

Supplemental Cash Flow

The final section that a company can have is the supplemental cash flow. Not all companies will have this section. The supplemental cash flow is used to provide additional detail for certain items. Facebook’s statement lists non-cash investing and financing activities. These include interest paid and changes relating to income taxes.

Conclusion

While the information included is by no means conclusive, by performing some basic financial statement analysis, you can become a better investor.

Many people incorrectly believe that you need some sort of insider information to have an edge. The truth is all of the information is available. It’s just a matter of if you’re willing to take the time to find it.

Reading through a company’s 10-K may seem daunting at first, but once you understand the key sections it becomes much easier.

When you’re reading through them, take notes and determine which sections you find most beneficial. Get in the habit of writing down key numbers (for financial ratio analysis). Also, see which sections don’t provide as much insight. This way you can leverage that knowledge on future companies, making your review more efficient.

A very nice summary of financials statements and how to navigate them. Brings me back to my accounting courses and studying for the CPA exam.

And now a nervous twitch is happening thinking about studying for that darn CPA exam…

I remember those days! It wasn’t that bad, lol

Thanks for sharing this article.It refreshed my knowledge on accounting. I found this article very helpful and knowledgeable.

Thank you! Really glad you liked it.

Yes, I totally agree with what you said. I think that reading will help as understand the things that we need to know. Like learning financial analysis, we need to read more about it. I believe that your article is a source of knowledge about financial analysis. Thanks for sharing this.